Table of Content

This insurance protects the lender - ANZ, not you - if you default on your home loan and there’s a shortfall following the sale of the property. Generally speaking the higher your LVR, the more LMI will cost. Lenders do not assess the balance of your card when assessing your borrowing power. If you are making interest only repayments then enter the interest only period in years. If you are making normal principal and interest repayments then enter 0. A redraw facility will provide for greater financial freedom in the future if used wisely as a mechanism for reducing debt and building wealth.

Based on the combination of factors that you select, the loan repayment calculator will automatically adjust the interest rate per annum and estimate your repayments accordingly. Estimated repayments are calculated on a monthly basis by default, but you can adjust the frequency to weekly or fortnightly if you’d like to compare the difference. Interest rate with special offer discountdisclaimerwhen borrowing 70% or less of the property valuedisclaimeron owner occupier home loan with principal and interest repayments. For interest only variable loans, the comparison rates are based on an initial 5 year interest only term. For fixed rate interest only loans, the comparison rates are based on an initial interest only period equal in term to the fixed period.

Owning costs – ongoing

The Federal Housing Administration is an agency of the U.S. government. An FHA loan is a mortgage loan that is issued by banks and other commercial lenders but guaranteed by the FHA against a borrower’s default. If you are renting a space, the monthly rent you pay is factored in. The total loan amount, interest, term, and repayment are considered if you have a current mortgage. But if you live with your parents rent-free or are a homeowner, you do not have a repayment or rental expense, which boosts your borrowing power. ' Calculator is only an estimate of how much you may be able to borrow.

My Maximum Purchase Price Calculate the maximum purchase price for buying a home. Compare your serviceability and deposit to find out if you can afford the mortgage.Saving For A Home Deposit Learn to budget and save for your home deposit. Factor in your costs & expenses, develop a savings plan and improve your borrowing power. Keep in mind that the interest rates in the calculator are subject to change, which can impact on repayment amounts.

Insurance

If your down payment is less than 20 percent of your home's purchase price, you may need to pay for mortgage insurance. You can get private mortgage insurance if you have a conventional loan, not an FHA or USDA loan. Rates for PMI vary but are generally cheaper than FHA rates for borrowers with good credit. It does not constitute a loan approval, quote or an offer to lend.

Eligibility criteria apply to special offer discounts, including $50,000 or more in new or additional ANZ lending. If you choose interest only, the minimum payment amount on your loan will be lower during the interest only period because you are not required to repay any of the loan principal. You will have to repay the principal down the track and so you may end up paying more over the life of your loan. There may be additional restrictions on the amount you can borrow or loan type you can select if you choose to pay interest only. A comparison rate is designed to help you work out the total cost of a home loan by building the known costs like up-front and ongoing fees into that rate. It doesn’t include things like government charges, redraw fees or fee waivers.

How Can I Improve My Borrowing Power?

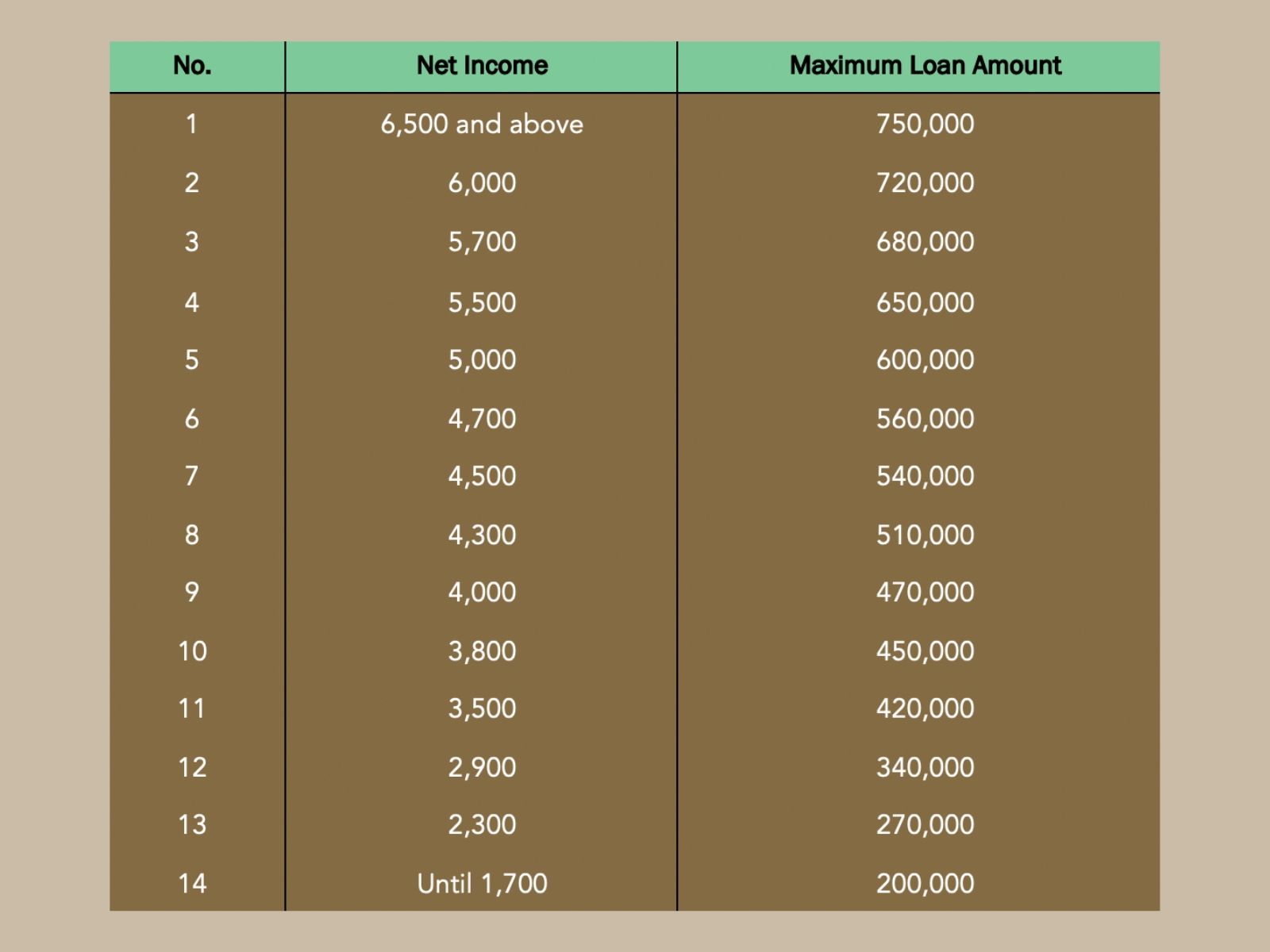

Generally speaking, your borrowing power is calculated as your net income minus your expenses. Your expenses can be impacted by things like the number of dependents in your family, any current home or personal loan repayments and other financial commitments such as private health insurance. The more accurate the details you enter into the calculator, the more realistic your estimated borrowing capacity is likely to be – so you may want to start by understanding your expenses.

The first stage of buying a home involves reviewing your finances to understand what you can afford to spend. If you already have a home loan with ANZ you can apply for a top up through the 'Apply and Open' tab in ANZ Internet Banking or goMoney . If you have a home loan with ANZ, you can apply for a home loan top up.

Banks ask for your housing situation to estimate the amount of money you’re likely to spend on housing each month, which will be factored into your borrowing capacity. Some banks have errors in the tax rates that they are using. They are usually very minor errors; however, we’ve copied those errors into our calculator so that we get the same results as the banks. Lenders will assess your taxable and tax-free income to calculate your borrowing power. Family Tax Benefits (A & B only), Centrelink payments, pensions and other tax free income can be entered here.

You should obtain a formal approval from a lender before making any offer on a property or any financial decision that relies on a new home loan. The monthly repayment you will be making on the property you want to buy is also factored in when calculating your borrowing power. If you have dependants on your loan application, the lender will calculate a lower borrowing capacity.

It is based on certain available information and is not a valuation of a property or guarantee of its market value or future sale price. Price ranges and predictions may change daily and the actual sale price may be different. The rate shown is the Simplicity PLUS Home Loan index less the applicable special offer discount.

When you're ready, you can apply for pre-approval online or an ANZ Home Loan Coach can help you work through the process. ’ calculator doesn’t take all of these lenders into account, it does compare three of the top lenders. The amount that you can borrow can vary significantly among different lenders. To make it even easier for you to use and understand our calculator, here is more information about some of the details you must enter to see your borrowing power.

Generally speaking, home buyers will need at least 5% to 10% of the purchase price as a deposit. Do you know how much deposit banks require for a home loan? We look at what lenders assess, budgeting, and how that impacts borrowing capacity.How Your Dependents Impact Your Borrowing Power How do your children affect your borrowing power? Learn about this and more on how you can improve your borrowing power without having to pay more.Improve My Borrowing Power Your borrowing power depends on your income, family size, and more. Find out how lenders calculate it and how you can improve it.Living Rent-Free Letter Living rent-free with your parents? Some lenders require a letter as proof for a home loan and may still charge a notional rental expense.

No comments:

Post a Comment